LIMITED SPOTS

All plans are 30% OFF for the first month! with the code WELCOME303

LIMITED SPOTS

All plans are 30% OFF for the first month! with the code WELCOME303

LIMITED SPOTS

All plans are 30% OFF for the first month! with the code WELCOME303

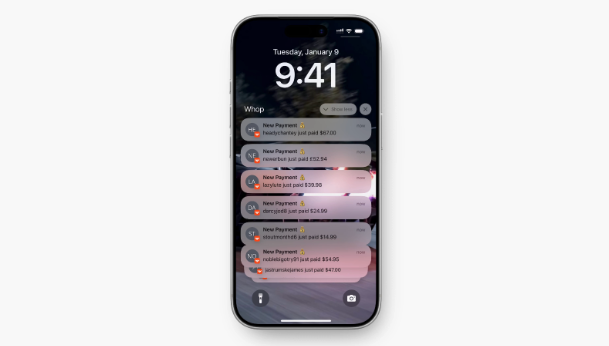

Whop gives SaaS founders subscription billing and license-based access control without writing custom infrastructure, and gives agencies client portals, invoicing, and retainers in one system. Its all-in card fee of 2.7% + $0.30 undercuts a Stripe Billing setup, at the cost of some low-level control. Here's how to decide which trade you want.

Whop works as the billing and access layer behind your software. Subscriptions, free trials, and tiered pricing come ready-made, so nobody on your team writes billing logic, dunning flows, or proration edge cases from scratch.

Access control is the underrated part. After purchase, each user gets a unique license key tied to their email login, and Whop's SDK exposes a method that checks whether a given user has access to a given product. Gating features by subscription tier becomes an API call rather than a custom auth-and-entitlements system, which is typically weeks of engineering work to build and a permanent liability to maintain. Official SDKs ship in JavaScript/TypeScript, Python, and Ruby for teams that want to integrate deeper than a hosted checkout link.

A minimal access check looks like this in practice: your app receives a request, you call the SDK with the user's ID and the product ID, and you get back a yes or no. That's the entire entitlements layer.

Most SaaS founders default to Stripe, so let's put real numbers on the comparison. Stripe charges 2.9% + $0.30 for card processing, and Stripe Billing adds 0.7% of billing volume for the subscription layer (recurring billing, smart retries, dunning). That's 3.6% + $0.30 all-in for a subscription business.

| Monthly revenue | Stripe + Billing (3.6% + $0.30) | Whop base (2.7% + $0.30) | Whop + billing add-on (3.2% + $0.30) |

|---|---|---|---|

| $10,000 (200 subs) | $420 | $330 | $380 |

| $50,000 (1,000 subs) | $2,100 | $1,650 | $1,900 |

| $200,000 (4,000 subs) | $8,400 | $6,600 | $7,600 |

The percentage gap is modest. The real difference is what you don't build: access control, license management, global payout rails, and BNPL support come included rather than assembled from parts. Against that, Stripe gives you more granular control over every billing edge case, a larger ecosystem of integrations, and no platform between you and your customer records.

The honest rule: if your billing requirements are genuinely unusual, build on Stripe. If you'd rather ship product than maintain payments infrastructure, Whop is the shortcut, and the fee math slightly favors it too.

Already live on Stripe? The switching cost is lower than you'd expect. Whop Migrations transfers existing Stripe subscriptions and payment tokens in one step, so current customers keep getting billed without re-entering card details. Involuntary churn from a billing migration is usually the reason SaaS companies stay put; removing it changes the calculation.

Agencies use Whop across the whole client relationship rather than just at the invoice. Case studies and templates go in the Files app to warm up leads. Signed clients convert to a one-time project fee or a recurring retainer. Each client can get a private portal with chat, files, and scheduling, which keeps communication and billing in one system instead of scattered across email, an invoicing tool, and a project tracker.

For agencies billing internationally, the payments layer does real work: local acquiring in the US, EU, Canada, Australia, and the UK means overseas clients' cards clear as domestic charges, and automated tax handling removes the multi-jurisdiction remittance problem. An agency invoicing clients on three continents normally absorbs that as manual accounting work; here it mostly disappears.

SaaS companies and agencies often hold meaningful balances between payout cycles. Whop Treasury lets that balance earn a variable yield, currently up to 6% APY, compounding continuously with no lockups.

Be clear about what this is before turning it on. Balances are held in USDT, a dollar-pegged stablecoin issued by Tether, and the yield is generated through the Aave lending protocol. The rate is not guaranteed and none of it is FDIC insured. For revenue that would otherwise sit at zero it's a legitimate option, but it's a yield product with crypto-infrastructure risk, not a savings account. Size your exposure accordingly.

Whop is built for speed and consolidation, so the main question is whether that matches your situation. If your billing is highly bespoke (usage-based metering with complex aggregation, negotiated enterprise contracts with custom terms), Stripe's lower-level primitives may fit better; Whop is optimized for getting standard subscription models live fast. Agencies already running a full CRM like HubSpot should map where Whop's client portal fits alongside it, since some functions will overlap. And as with any platform, from Stripe to Shopify, your billing and access control run on Whop's infrastructure, so weigh that the same way you would any core vendor.

Can Whop handle free trials and tiered pricing? Yes. Trials, tiers, and one-time purchases are configurable per product without custom code.

Which languages do the SDKs support? JavaScript/TypeScript, Python, and Ruby, all official.

How do payouts work for agencies with international clients? Clients pay in their local currency through local acquiring where available; you withdraw via ACH ($2.50), wire ($23), or instant payout (4% + $1).

Is Whop Treasury safe? It's powered by an established lending protocol and a major stablecoin, but it is not FDIC insured and the rate is variable. Treat it as a yield product, not a bank account.

For a SaaS founder, Whop is the fastest route from product to billed, access-controlled customers, and the all-in fee beats a Stripe Billing stack at every revenue level in the table above. For an agency, it consolidates lead nurture, client portals, and recurring invoicing into one system. Choose Stripe when control is the priority; choose Whop when speed is, and know exactly which one you're optimizing for before you integrate either.

Send emails at scale

Send emails at scale